Summary

- Japan’s strengthened fiscal mandate is lifting global rate expectations and tightening marginal liquidity, creating a structural headwind for high-beta assets including crypto.

- Strong US labor data alongside moderating inflation have reinforced expectations of no change at the March FOMC meeting, with the first rate cut window now pushed to summer.

- Leverage remains elevated despite recent liquidations; BTC-term OI stays high, leaving the market structurally fragile.

Policy Changes and AI Pressures on Markets

Japan: Policy Mandate, Rates & Global Liquidity

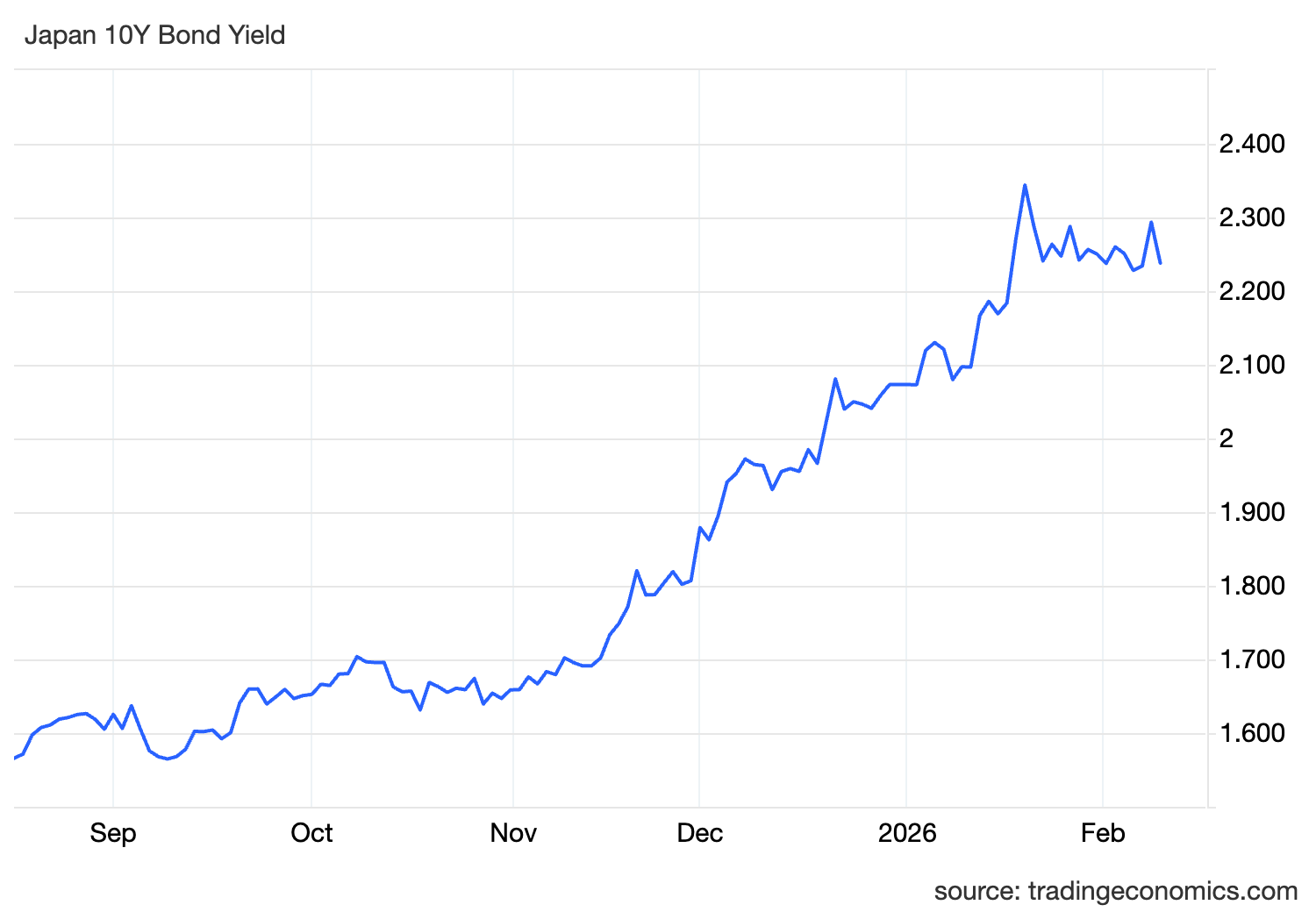

In the Feb 9 nationwide vote, Japan’s ruling Liberal Democratic Party and its coalition partners secured a decisive victory in the House of Representatives, winning a majority of the 316 seats and achieving a two-thirds supermajority in the lower house for the first time. This result grants Prime Minister Sanae Takaichi a strong policy mandate and materially increases her ability to pursue a more aggressive fiscal expansion agenda.

Markets reacted quickly to the shift in fiscal expectations. Anticipated increases in Japanese government bond supply pushed yields higher across the curve, with both the 10-year benchmark and short-dated rates moving up. Japan is no longer treated as a permanent low-rate anchor, raising global funding costs and reducing certainty around future financing conditions.

Under this new rate and liquidity regime, global capital flows are adjusting structurally.

- Japanese domestic assets have become more attractive, prompting signs of institutional capital repatriation

- JPY carry trades are shrinking, reducing the availability of cross-market high-risk capital

- Emerging markets face greater pressure from capital outflows and rising volatility

For crypto assets, these developments constitute a short- to medium-term liquidity headwind. As marginal risk appetite weakens, crypto, as a high-beta asset class, is more likely to come under pressure.

Equities: SaaS De-rating under AI Pressure

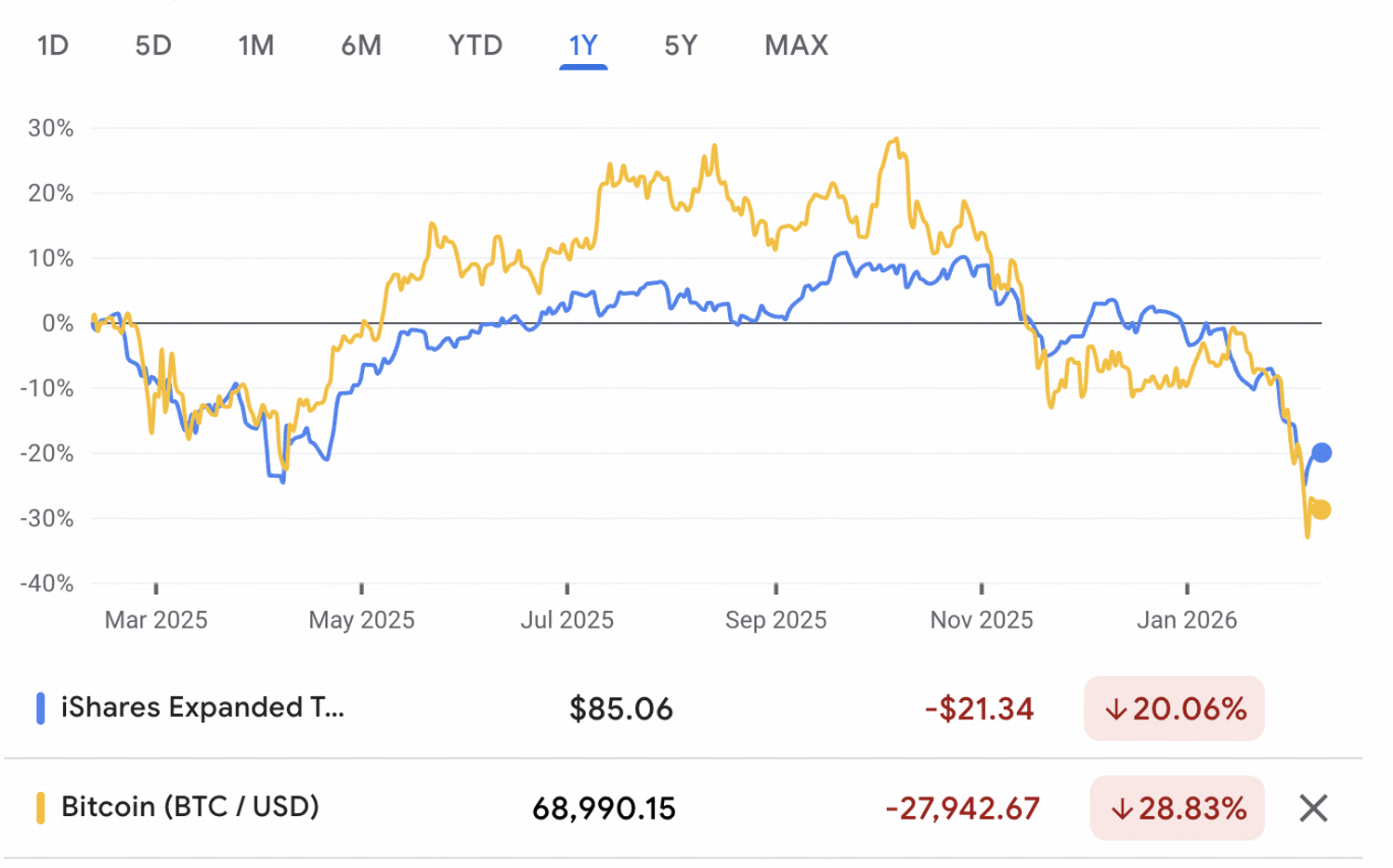

Equity markets have seen a sharp sell-off in high-growth software stocks. The software and SaaS sectors have undergone a clear valuation reset, with the U.S.IGV ETF, which represents the software industry, serves as a proxy for this broad-based SaaS downturn. The ETF has fallen more than 20% from its peak, highlighting the severe drawdown across SaaS and cloud computing stocks.

The underlying drivers are straightforward. Markets are increasingly concerned that AI may fundamentally erode the SaaS business model.

- AI’s growing capabilities may replace or commoditize certain software services.

- Integrating AI into existing products has become a costly burden, undermining the high-margin profile that SaaS companies have historically relied on.

In short, AI has shifted from a tailwind to a source of margin pressure and competitive threat. These concerns have been rapidly reflected in valuations, with investors aggressively de-rating software stocks. Even SaaS leaders such as Salesforce (CRM) have not been spared, as heightened uncertainty around growth prospects and rising costs has led markets to demand meaningfully lower valuation multiples.

The chart highlights a clear similarity between Bitcoin and the IGV software ETF over the past year, including declining at the same time into early 2026.

This co-movement is noteworthy. As suggested by another analyst, “Bitcoin is just open source software.” If segments of TradFi investors frame BTC within the broader software complex, they may simply trade it in line with that trend. This spillover dynamic could be one contributing factor behind Bitcoin’s recent weakness.

US Jobs & CPI Data Shift Fed Rate Outlook

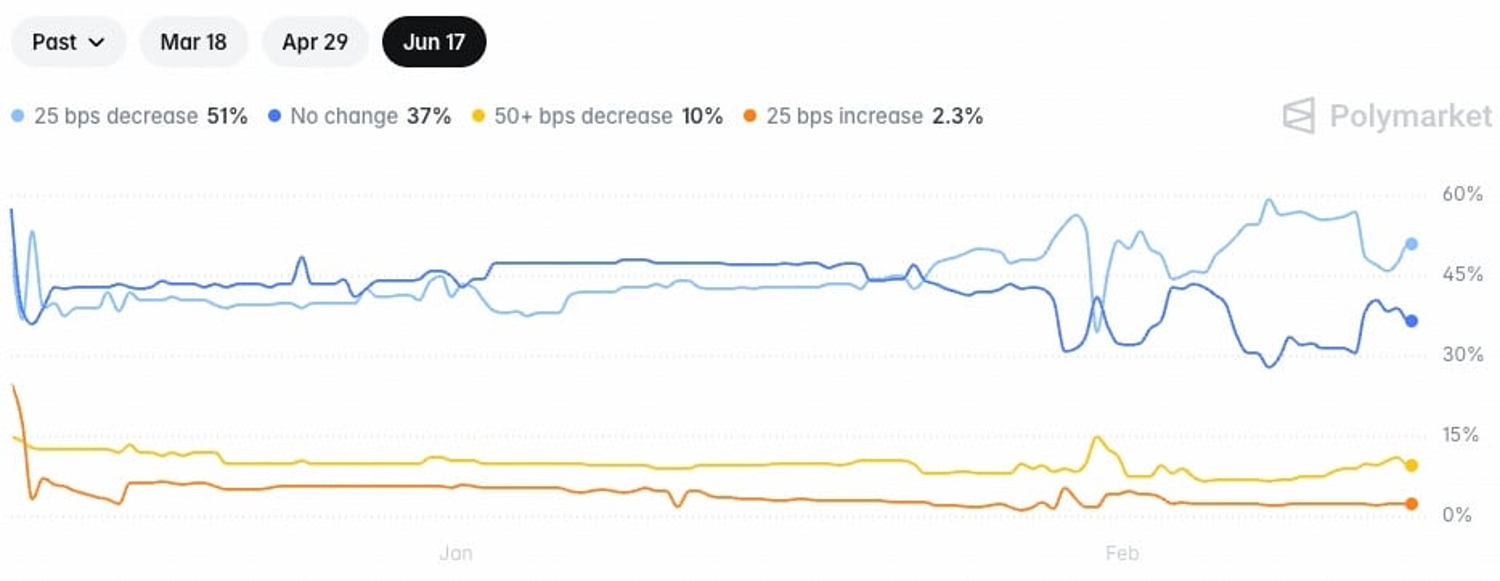

US January nonfarm payrolls surged by 130,000, far exceeding expectations and signaling a resilient labor market with unemployment steady at 4.3%, which initially bolstered the dollar and pressured risk assets like cryptocurrencies. Meanwhile, headline CPI cooled to 2.4% yoy and core CPI eased to 2.5%, marking multi-year lows and reinforcing disinflation trends.

The combination of solid macro data, particularly the strong January jobs report, and the nomination of Kevin Warsh as potential Fed Chair has driven market expectations firmly toward the Fed holding steady at the March meeting, with the probability of no rate change now at around 94%, pushing the first rate-cut window likely to summer.

Currently, markets are pricing in more than 60% odds of a rate cut by the June meeting.

Flow: Resilient Stablecoins and Subdued Buying Flows

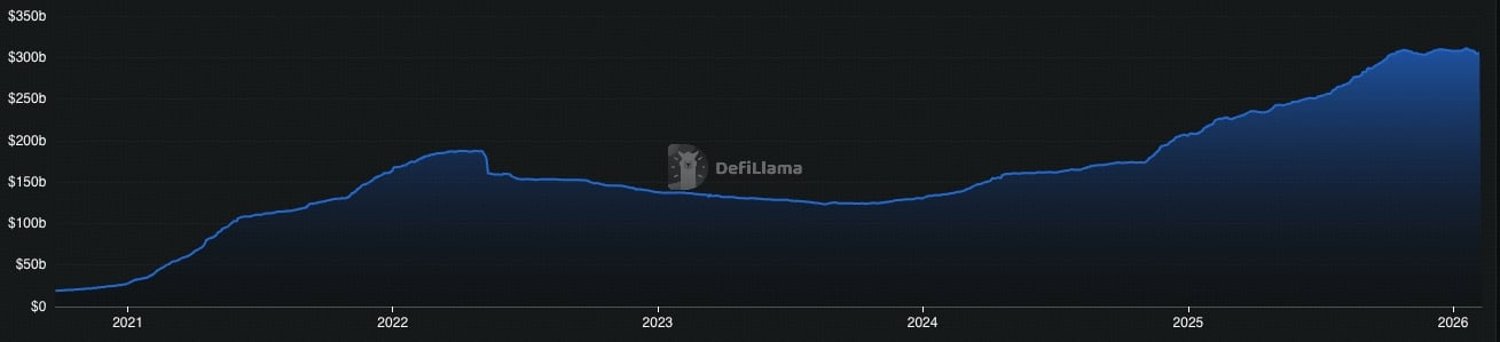

Despite Bitcoin’s roughly 40% drawdown in February 2026 from its late-2025 peak, total stablecoin supply has remained broadly stable, with only minor fluctuations during the sell-off.

This stands in clear contrast to prior cycles, where drawdowns of similar magnitude were typically accompanied by large-scale stablecoin redemptions, depegging events, and capital exiting the crypto ecosystem altogether.

The key reason lies in the maturation of the stablecoin ecosystem. By 2026, stablecoins have evolved into multi-functional financial instruments. Stablecoin usage has expanded well beyond trading pairs, increasingly serving as vehicles for cross-border payments and value storage.

As a result, the relationship between stablecoin flows and market drawdowns has structurally changed. Stablecoins are no longer exiting the system during stress episodes; instead, capital has rotated within crypto. When market conditions stabilize and risk appetite recovers, this sidelined liquidity can once again translate directly into renewed purchasing power.

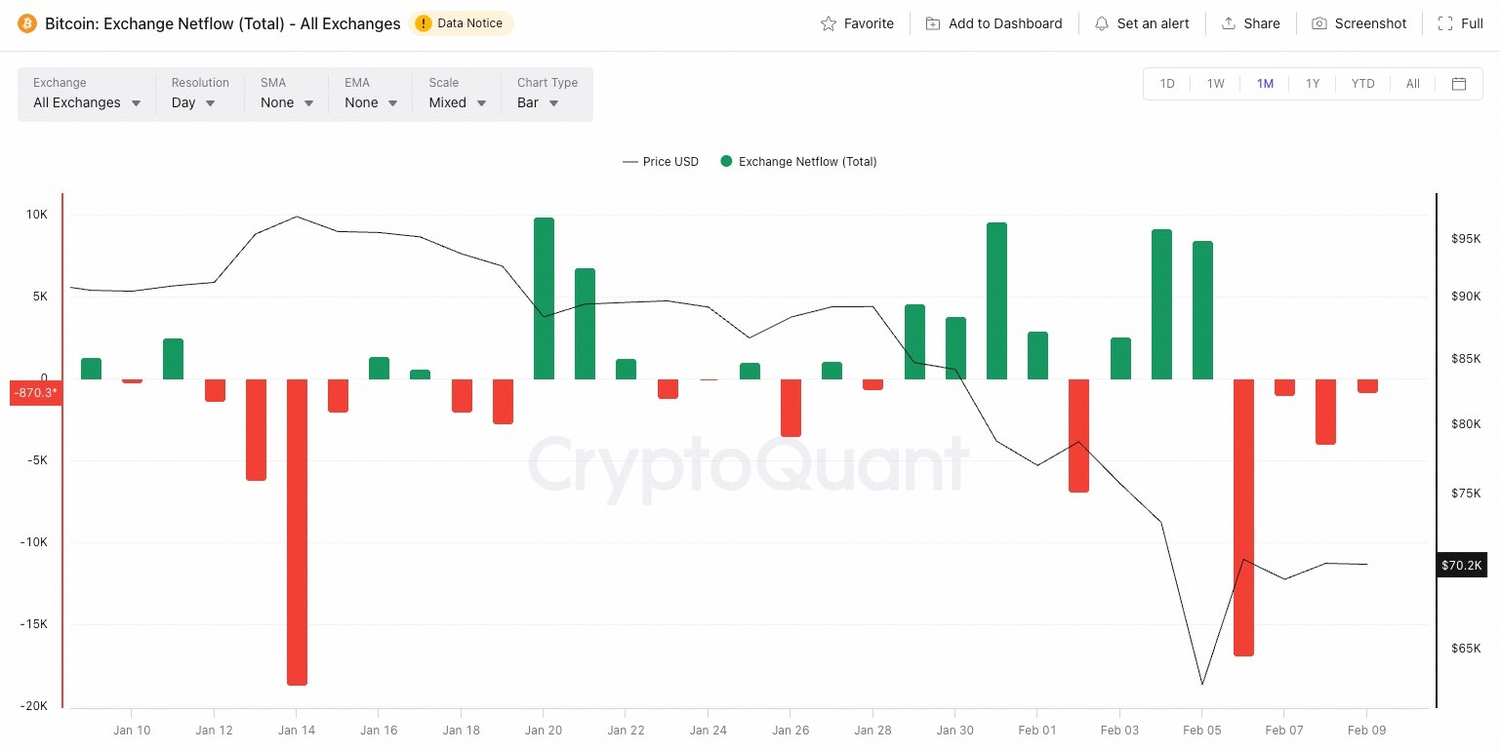

Weak Sustained Flows After the Decline

During the sharp price decline on February 6, Bitcoin exchange netflows recorded significant outflows, showing that some investors actively accumulated BTC at lower levels and moved coins to self-custody. However, these outflows diminished rapidly on February 7-8, indicating that the initial accumulation momentum was short-lived and buying interest quickly cooled.

Complementing the on-chain picture, Bitcoin Spot ETF flows revealed limited institutional participation. Weekly net inflows turned substantially negative around the decline (reaching -$689M in the recent week), reflecting significant net outflows and weak institutional buying support. Together, these signals suggest overall subdued confidence and limited accumulation at current price levels.

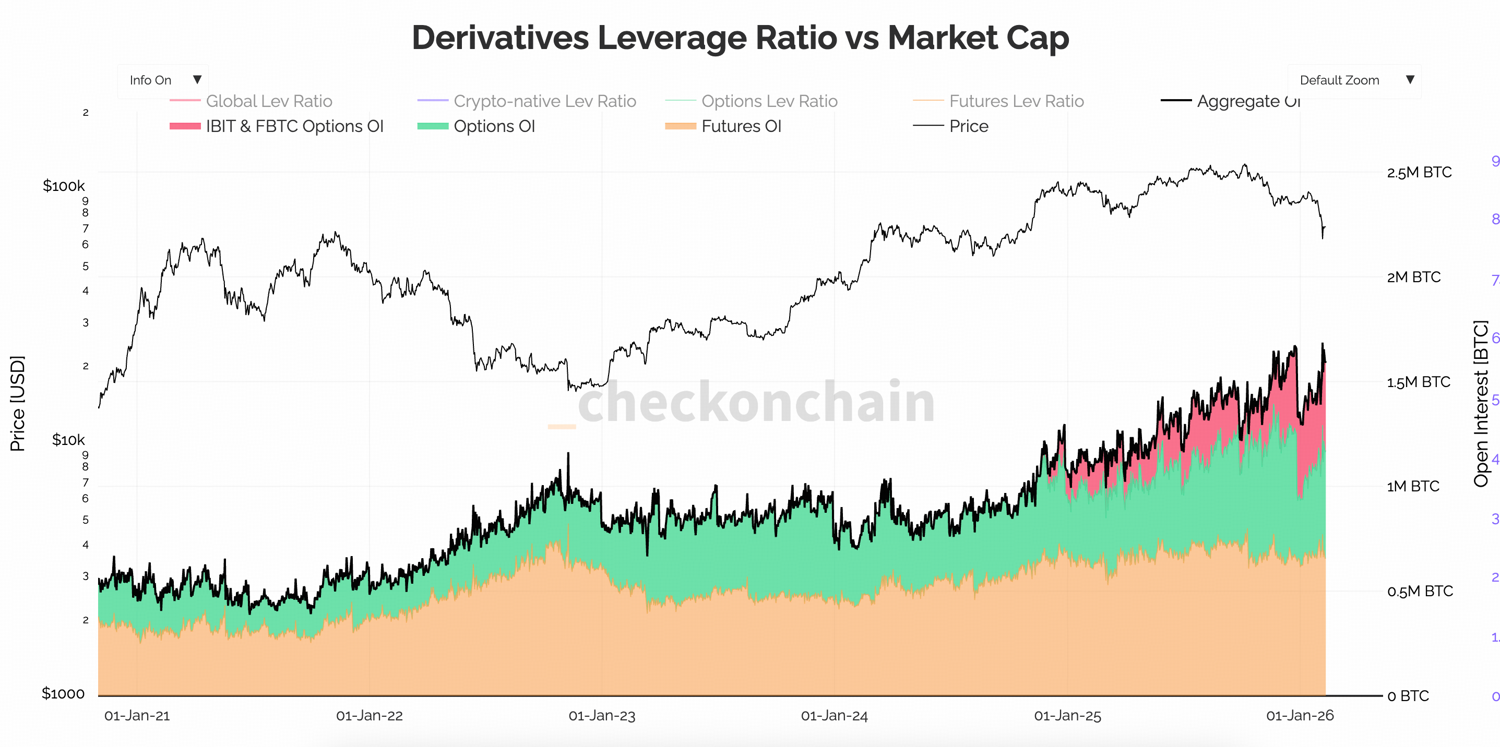

Derivatives: Leverage Has Rotated, Not Cleared

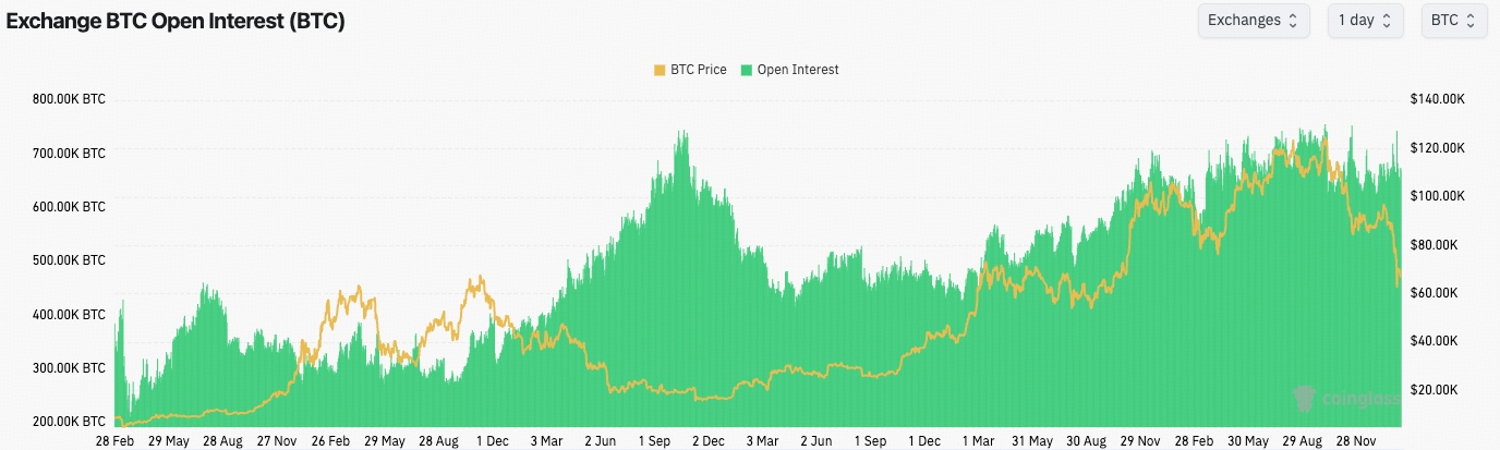

At first glance, recent volatility appears to have triggered meaningful deleveraging. BTC futures open interest measured in USD terms declined sharply during the selloff, suggesting leverage was reduced.

However, when open interest is measured in BTC terms, the contraction is far more limited and remains elevated relative to prior cycles. This contrasts with 2022, when OI in BTC terms fell sharply during the crash, reflecting genuine position unwinds. In February 2026, OI in BTC terms has not shown a comparable collapse, suggesting that the decline in USD terms reflects price effects more than true deleveraging.

The distinction is critical. BTC-term OI removes price distortion and captures changes in actual contract size. If BTC-term OI remains high, it means leverage remains embedded in the system, even if USD notionals appear lower.

This cycle has also expanded the derivatives complex through ETF-linked products such as IBIT-related instruments. Even after the recent liquidation wave, aggregate leverage remains elevated compared to earlier stages of the cycle.

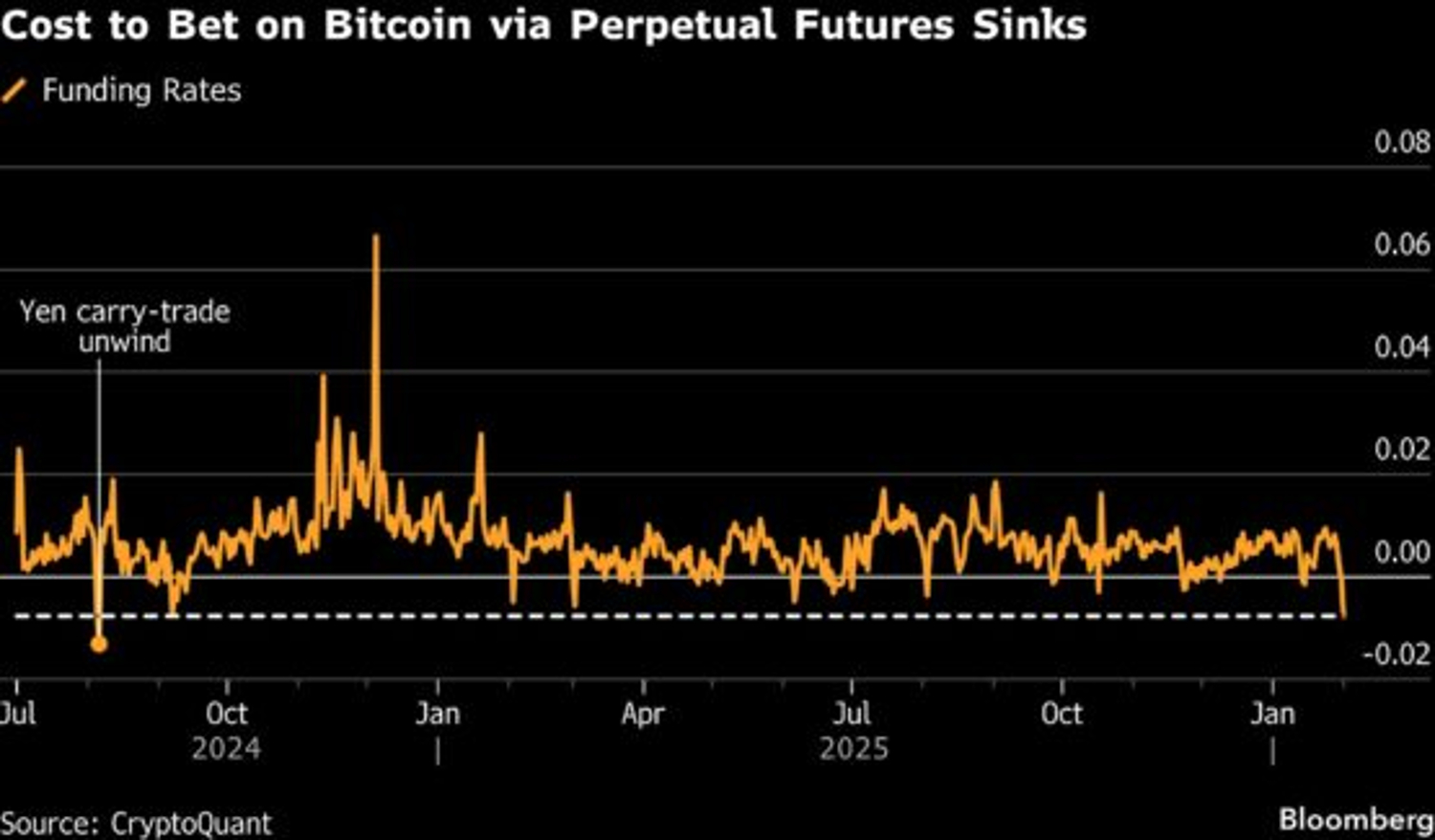

Funding rates have shifted toward neutral to slightly negative. The decline in funding reflects reduced willingness by longs to pay for leverage, indicating a market that has moved toward balance or a mildly bearish bias.

Derivatives Takeaway

- Leverage remains elevated.

High BTC-term OI shows that contract exposure is still substantial despite the recent liquidation wave.

- Positioning has rotated, not exited.

Funding near neutral suggests long exposure was reduced but largely replaced by shorts and hedged structures.

- Fragility remains embedded in the system.

Elevated BTC-term OI implies forced flows can still be triggered in either direction.

Week Ahead

- Feb 14 FTX Creditor Distributions

- Feb 17–21 ETHDenver 2026

- Feb 18 FOMC Minutes: Jan 27–28 meeting

- Feb 20 U.S. GDP (Advance): 4Q & full-year 2025

Next week combines liquidity-sensitive macro events with crypto-specific catalysts. FTX creditor distributions on Feb 14 may create short-term supply pressure, while ETHDenver could influence sentiment around the Ethereum ecosystem. On the macro side, FOMC minutes and the U.S. advance GDP release will shape rate expectations and growth narratives, keeping markets highly sensitive to liquidity and positioning shifts.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.